There are two ways to find low interest mortgage rates between 2-4%. First and foremost you will need to locate an assumable mortgage in the area you are looking to buy your home. Once you find a property, simply ask the seller. However, the easiest way to get all of this data at once is to order a Interest Rate list of assumable mortgages from us. This assumable strategy is a home buying technique that allows buyers to take over the remaining payment term and rate. These homes are off market assumable mortgages, were established when rates were lower than 5%, and the list helps buyers get in front of the competition to prevent bidding wars.facts

Home Buying 101

- Find the lowest Interest Rate Mortgage

- Find the shortest payment term

- Bypass as much closing & settlement cost as possible

- Avoid bidding wars, by getting there first

Assumable mortgage – A mortgage that can be transferred with no change in terms. Most VA/FHA/ & some Adjustable Rate loans are assumable. We have the tools to help you verify if any loan is assumable.

- FHA Assumable Mortgages – All FHA mortgages made after December 14, 1989, can be assumed. All FHA mortgages made before December 1, 1986 are assumable. This means there was only 3 years where FHA mortgages were not assumable. These FHA Mortgages can be assumed with a buyer credit approval. See HUD facts here HUD General Assumption info doc or See page 710 of the FHA Handbook

- VA Assumable Mortgages – Any VA mortgages made before March 1, 1988, is assumable. The buyer must be credit qualified. If the seller is a veteran, they should confirm how this will affect their VA eligibility.

- Conventional/ARM (Adjustable Rate Mortgage) – Adjustable-rate mortgages first appeared in the 1960s but did not gain wide popularity until the 1980s. These Adjustable Rate Mortgages are based on the US Treasury weekly average yield. It includes a 1yr maturity published weekly by the Federal Reserve. Sellers should contact their lender directly to confirm assumability.

Low equity can be determined by the property LTV.

Technically – The loan-to-value ratio is a metric lenders use to determine their risk of loaning money. The higher the ratio, the higher the risk. It simply is the resulting figure after comparing the market value of the property vs the amount owed against the mortgage. Normally most mortgage loans are considered safe (not at risk) when the loan to value ration is 80% or less. While the ratio is a percentage, LTV is calculated by dividing the original mortgage amount by the current property value.

Of course positive VALUE means EQUITY/PROFIT margin. The sweet spot for Assumable mortgages is NEGATIVE VALUE. Persons with Assumable mortgages are more likely to have an assumption conversation. When shopping for an assumable mortgage, locate a property on your list that does not have any or much equity. These will be properties that have high loan to values (LTV). Anything higher than 85% is a good place to start. High LTV is also referred to as Underwater Mortgages, short sales, negative equity, and some times may even be called distressed properties. It essentially means they owe more than its worth.

- Express interest – Schedule a consultation. Contact the seller to express interest. Wait for the owner to respond. Make arrangements to view the property. Confirm your credit rating is above 600. Discuss the current loan details with the seller. Request assumption package – Sellers must contact the lender directly to request an assumption package. This package will tell the buyer everything they need to do and everything both can expect during the process.

- Review – Review the exact terms of the loan. When assuming a mortgage, you need to make sure that you understand everything. Ask the lender about the specific requirements to move forward. You may also need to credit qualify for the loan. Some lenders may ask for a small amount to secure the loan. To avoid surprises, buyers should review the due on sale clause. If the seller is delinquent, but not in foreclosure, you may be required to pay the past due amount. This language would be located in the “due on sale clause”.

- Inspect – As a protection, we suggest you have the home inspected before you buy it.

- Sign – Before signing anything, it is vital that you read over every piece of paperwork and you completely understand everything. Consider if you need to pursue a second mortgage to make up any pricing differences. Then provide the lender with the required documentation.

- File – Sellers should keep the release of liability documents received from the lender, as it will protect them in case the new borrower defaults.

Disclaimer – Many owners are not aware their property is assumable and need guidance. Takelist cannot guarantee the prospective owner will respond. Nor can we promise they will start or complete the assumption process.

It is a standard practice to pay the seller whatever amount of equity there is in their property. In cases of large amounts of equity (any figure above 4% of the home value), we would recommend using a realtor or lawyer or title company to facilitate the process as a financial protection. They can charge as little as 1 to 2% to facilitate a transaction, but not always.

There are multiple resources.

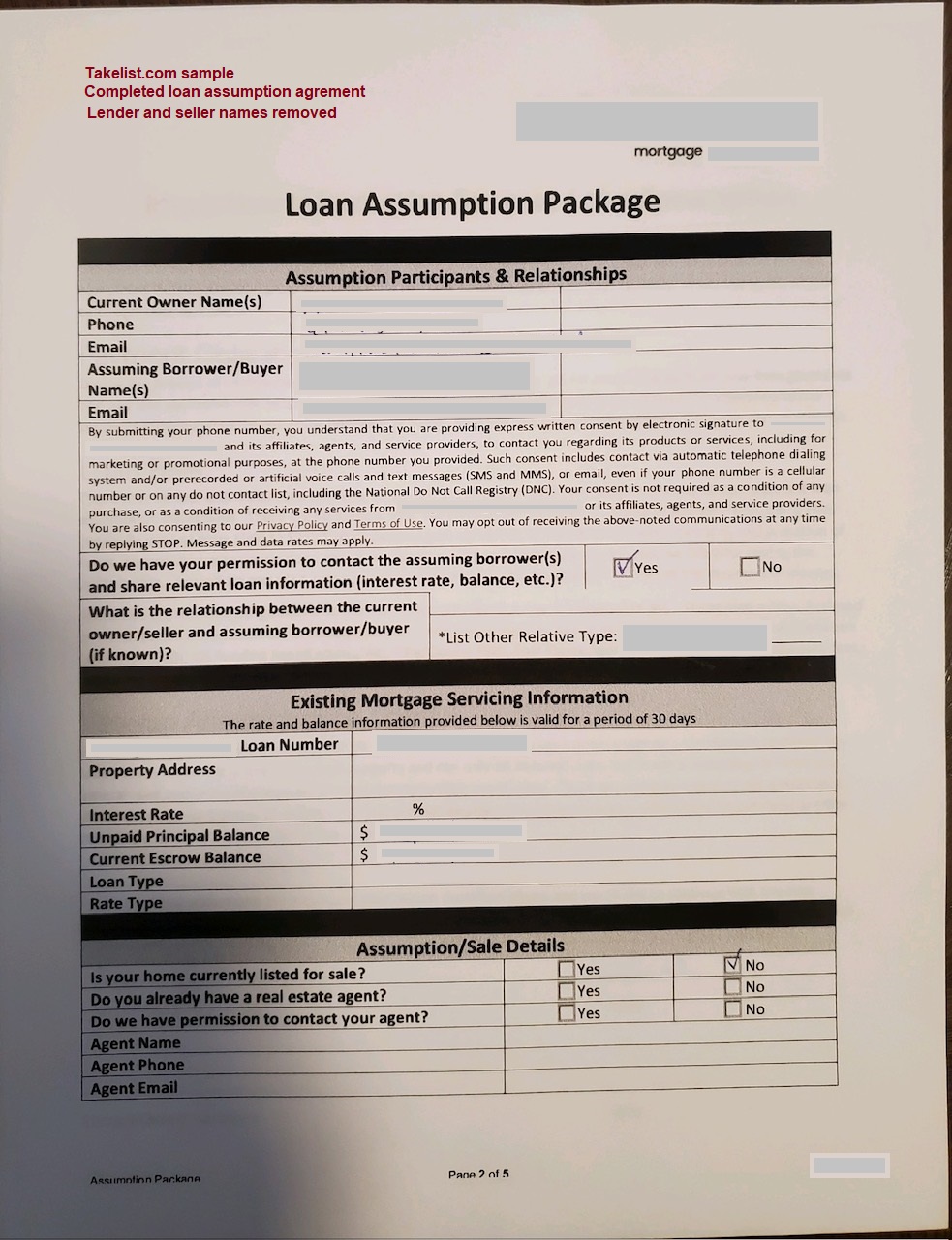

Here is a 1 page example from a recent Lender and Seller Assumption Package.doc.

{kind=link}

Here is a link to the HUD Document that shows the instructions (See page 2).

Here is a link to all Legal HUD sample forms.

- Sample – FHA Loan – Assumption Package & Release of Liability document.

- Sample – VA Loan – Assumption Package & Release of Liability document.

One more thing to remember – Transfer the Liability properly.

During the Assumption process request the lender to modify the original contract. “Put the buyer in your place as the person primarily liable for payment of the mortgage”. Modifying the obligation to pay the mortgage will completely discharge you of liability

Figuring out where to draw the line between what’s private and what isn’t becomes clearer once a person understands the difference between a mortgage record and a promissory note. They are two separate things. Mortgages and deeds of Trust are definitely public records because it is a real estate transaction. Lenders must provide details to the government regarding the financing they approve or originate to comply with FFIEC HMDA guidelines. One item on the list include the interest rate. Even though a person may highly regard their mortgage data as very private, the information is shared to monitor discrimination in the financial sector. A promissory note on the mortgage is not public record and so doesn’t get filed with any government authority. Turns out a good amount of what is in the promissory note is also in the mortgage record reported to the government. Maybe that in itself seems somewhat senseless, but that’s how its set up for now.

Since 1934 the largest insurer of residential mortgages in the world, has over 70 million assumable properties. Acquiring a list of assumable mortgages is the first step to getting into one of these properties. Below are a few of the benefits of pursuing an assumable property before it goes on the market for sale.

FACTS

- Save 5 -10 years of mortgage payments.

- Acquire a low interest rate mortgage between 2-5%

- Bypass escrow fees, document fees, appraisal fees, points and brokerage commissions.

- Own a proprietary list formulated for Assumptions. Some of the data includes home specs, assumable mortgage property details, owner contact name, property address, phone, 100% opt-in email, and more.

There are many assumable homes in the market that are not yet listed on the market by realtors and other liscenced professionals. Their list is different from our list. Realtor list display homes for sale with transactions that require settlement cost. Our private list is not a list of homes for sale, but helps you to “make contact first and avoid all settlement cost”. While we cannot promise a sale, our Robust, Interest Rate, and Deluxe data list are current and verified by the government. The robust, interest rate, and deluxe list normally includes home specifics like the number of beds and bathrooms, Public Assumable Mortgage details, full contact name, address, 100% opt-in email, and in some cases could include the owners potential social handle information. Our Quick list data offers a more basic list of property addresses, names, and emails of owners with assumable mortgages.

After any purchase feel free to use our site tools, and complete our 8 steps to assume a home. We in-turn will coordinate with you the use of our free automated tools that can help trigger the initial assumption discussion.

By scraping public records, third-party data companies can assemble thousands of attributes for billions of people. This allows them to capture Loan Type -Home Owner Name -Postal -Property Type -Original Loan Amount -Original Loan Date -LTV -Loan Interest Rate -Number of Bathrooms -Number of Bedrooms -Potential Homeowner phone -Potential Email -Potential Social handles We append this list to ensure our clients receive data that is tailored to the Assumable marketplace.

There are several steps to consider. Step 1. Express interest in the property. Be ready to say the right things to the owner. Our consultation is highly recommended as it prepares you for this. Step 2. Respond to homeowner interest. To learn how to properly respond to homeowner interest please use our consultation service. Private list pricing Many owners are not aware their property is assumable and need guidance. We cannot guarantee the prospective owner will respond. Nor can we promise they will start the assumption process. Our Assumable marketing administration tools are designed to help you make the initial contact with the home owner. You can select pre-tailored phone/mail/ messages.

This is our full service package which includes all of the services available in our directory. Our team will consult with you, locate and present a list of assumable property options based on your desired criteria. With your permission we will coordinate the first 5 of 8 easy steps of the assumption process with you. 30% of the Assumable Facilitation Service is required upfront. The remaining expense will be transacted once the assumption is complete. Overall there are 3 stages to our facilitation service. It is billed in 3 stages to give our customers control over advancing through each stage. 1-Stage A: Consultation $169* 2-Stage B: Deluxe List $599* 3-Stage C: Facilitation service $959* service & pricings are subject to change

Yes. This directory service is new. The strategy however is decades old. We are now the dedicated resource for finding assumable mortgages, and will continue to educate home owners and buyers of this option. Although this has been around for years, many do not know their mortgage is assumable, and can transfer it to someone who wants it. Buyers who need down payment assistance can use this strategy to minimize any-all up front cost.

This strategy is for: Buyers: Buyers with a FICO credit score of 530 or higher. Buyers who are willing to speak directly with the seller. Buyers who are looking to by pass all settlement fees, down payment cost, and years of mortgage payments. Home Owners/Sellers: Homeowners who have a FHA, VA or ARM loan, has little or no equity value in their home, or facing foreclosure, or has been asked to lower the selling price,or has been asked to take a loss by doing a short sale, or simply having a challenge selling their property through traditional sales methods.

Avoid all traditional cost associated with buying & selling a home. Release Seller liability, Preserve seller credit rating, Prevent exposure to any financial loss Shorter mortgage payment term No Down Payment Cost No Closing Cost Minimal paperwork No Bidding Wars Home Affordability No Appraisal Cost Prevent Tax loss Preserve credit score Convenient Signing process Assumable Advertising Power

It is a standard practice to pay the seller whatever amount of equity there is in their property. In cases of large amounts of equity (any figure above 4% of the home value), we would recommend using a realtor or lawyer or title company to facilitate the process as a financial protection. They can charge as little as 1 to 2% to facilitate a transaction, but not always.

Traditional buyers simply establish a second mortgage to cover a large amount of equity when they do not have enough cash to cover it.

When a Homeowner has equity, they can request the buyer to provide a cash payment for the difference between the loan amount and the value. Normally this is done with a loan when it is a large amount. Legal documents would be necessary to accomplish this. Traditional selling with an agent will cover this part in their title closing services. FSBO opportunities should use a title closing service to protect the interest of both parties.

- Home equity = The difference between the market value and the outstanding balance of all liens on the property.

- True equity = The amount you can capture in cash. This is normally received in a check when you close a loan. It is important to recognize that there is a difference between the two terms.

Example- Sellers who have little equity in their property should realize that even though it is called Home Equity, you will not be able to get 100% of it. Only a portion of it is the true cash equity. Home equity is appealing to buyers. True equity is appealing to sellers.

SELLERS – Posting your home on our directory makes it visible to hundreds of visitors per day. Buyers will contact you directly. Individual postings $59-$169 until it sells (12 Month max). Rates for posting multiple properties vary. BUYERS – Private Assumable List $119 – $299. Get their 1st data $12 each. Investor LTV list $800. Consultations $89-$199. Complete Assumable Facilitation Service $1500. All rates are subject to change.

Conventional loans that have a ARM (Adjustable Rate Mortgage) are assumable. Conventional loans that have a Fixed Rate includes a due on sale clause which requires the balance to be paid in full when the property is sold. Fixed rate loans follow the strictest guidelines for eligibility and are not assumable. Even if it is not assumable homeowners who have a Conventional mortgage can post their home if they are interested in offering a Contract For Deed option. Interested buyers will need to eventually establish their own financing. There is plenty of information for research online about this option. Here is a place to start

Pay Online Create user account: You must have a valid email address. Click Sell it or List it to begin. Pay: Your property will post in the directory immediately. A notification is sent to your email address with your login and password details. Maintenance: Conveniently make adjustments to your account information using the login and password details provided. Please be sure to delete the property when the sale is complete. Pay By Check To pay by check simply fill out the form below and mail it to the address listed. Customer Form – Download Mortgage Details You Will Need: Collect this additional data before processing: Loan type (FHA, VA, or CONV)* Current Balance* Monthly Payment* Bank Name Interest Rate Loan Year Term Term Years remaining* Market Value House Swap Option (yes/no) Contract for Deed option (yes/no) Required Item

We are a strategic resource for locating all assumable homes in the US. We offer a consultation service and a strategy that protects the financial interest of both the Buyer and Seller. We advertise the monthly payment instead of the purchase price. We help buyers locate homes before any mark up in price occurs. Assumable homes gain better visibility over other sites that are crowded with too many listings. Our clients have complete control over their property details and posting a home is simple. We are the only dedicated sales resource on the web for Assumable properties that have low or no equity. We provide a easy to use tool for sellers and buyers to connect directly.

Inflated housing prices and appraisal reviews were two major components that led to the 2007 economic downfall. In addition, several bank failures were the direct result of volatile mortgage lending. While it will take some time to undo the effects of these, transferring the sellers financing on to the buyer does resolves the issue of non performing mortgage loans, controls inflation, improves home affordability, and saves consumer credit ratings. These benefits can only be reaped by consumer action.

Yes. You can entertain multiple offers at the same time. In this scenario your lender will most likely accept the person who is most credit worthy.

Increase interest by marketing your property to buyers online. In today’s online world, curb appeal has taken on a whole new meaning. When buyers take a fresh look at your home through the eyes of the internet, you can invoke an emotional response. It will be positive if you have good photos. In fact, within the first 3 seconds the impression of your photos will determine a buyer’s interest. Since all buyers take curb appeal seriously, so should you. Stage, De-clutter, and brighten up your home before taking pictures. Then pick only the best shots before you post them online. Accentuate the positive and eliminate the negative.

There are many resources available online. We in fact are so confident in our service, we are happy to share credible competitor resources with you. Take a look and then Take advantage of our service today. Creditable Resource 1 Creditable Resource 2 Creditable Resource 3

Takelist.com can also be used as a House swapping resource. Relocating to a different city or state is important when you are changing business location or simply want to move to a warmer climate. In addition trying to buy “contingent upon selling” can be difficult. Some have even missed out on buying their dream home because they could not sell their current property fast enough. With us, its easy to team up with others who want to explore swapping homes. All homes clearly specify if the seller is optimizing a house swapping option. Once you post yours and they list theirs, you can contact each other to combine your efforts. How does this work? The entire process is the same for both properties. Each owner will need to credit qualify and complete each of the steps required by their lenders. Since each signing is separate and there is no obligation to either owner it would be best to schedule the signings on the same day. Check mark the House Swapping option if you are interested in relocating or need to sell before you can buy.

3 options Purchase a Consultation. Highly recommended before you begin making contact with the Owner. Purchase a Get There First property. Search and select individual properties to choose from. Purchase a Private Assumption list. Order a list of properties in your area. Choose from 3 private list options. Purchase Facilitation Service. This includes Consultation, private list, and facilitation of the assumption process.

Yes absolutely. To be eligible for an FHA loan as a small business owner, you must fit one of the following business structures: sole proprietorship, partnerships, limited liability corporation (LLC), corporation, or “S” corporation. You are only eligible if you own 25% or more of the business. Feel free to verify HUD’s Investment Property Eligibility and Underwriting in Section 4 Section B.

Related questions:

- Can I own more than 1 FHA loan. Answer = No. FHA loans normally have owner occupant guidelines. If however you are purchasing the additional property under a business name (as mentioned above), you can technically own as many as you can afford.

- Can I own more than 1 VA loan. Answer = Yes. The VA allows veterans to have two VA loans at the same time even if they’ve defaulted on one in previous years. This service is called “second-tier entitlement”.